Extending the Basis Trade to Commodities: An Analysis of Gold Perpetuals

In the recent post on diversifying USDe’s backing, we outlined multiple proposed extensions to the backing assets: overcollateralised institutional lending, real-world assets beyond T-Bills, and equity and commodity basis trades.

This post goes deeper on the third strategy: equity and commodity basis, and specifically the first asset under consideration, tokenised gold perpetual futures.

The logic for extending into commodity basis trades is a direct application of what Ethena already does. Ethena has operated one of the largest delta-neutral books in the industry for several years, applying the same methodology across BTC, ETH and SOL.

The same framework applies cleanly to any market with a liquid spot asset, a liquid perpetual futures market, and a structural funding rate premium. Commodity perpetuals, specifically gold, now meet those conditions at institutional scale.

Before any allocation is made, the Ethena Risk Committee completed a formal review of commodity and equity perpetuals, established a dedicated eligibility framework adjusted for these markets, and assessed gold-backed tokens against that framework. That work is highlighted in the below post.

The Risk Committee’s full analysis is published on the Ethena governance forum.

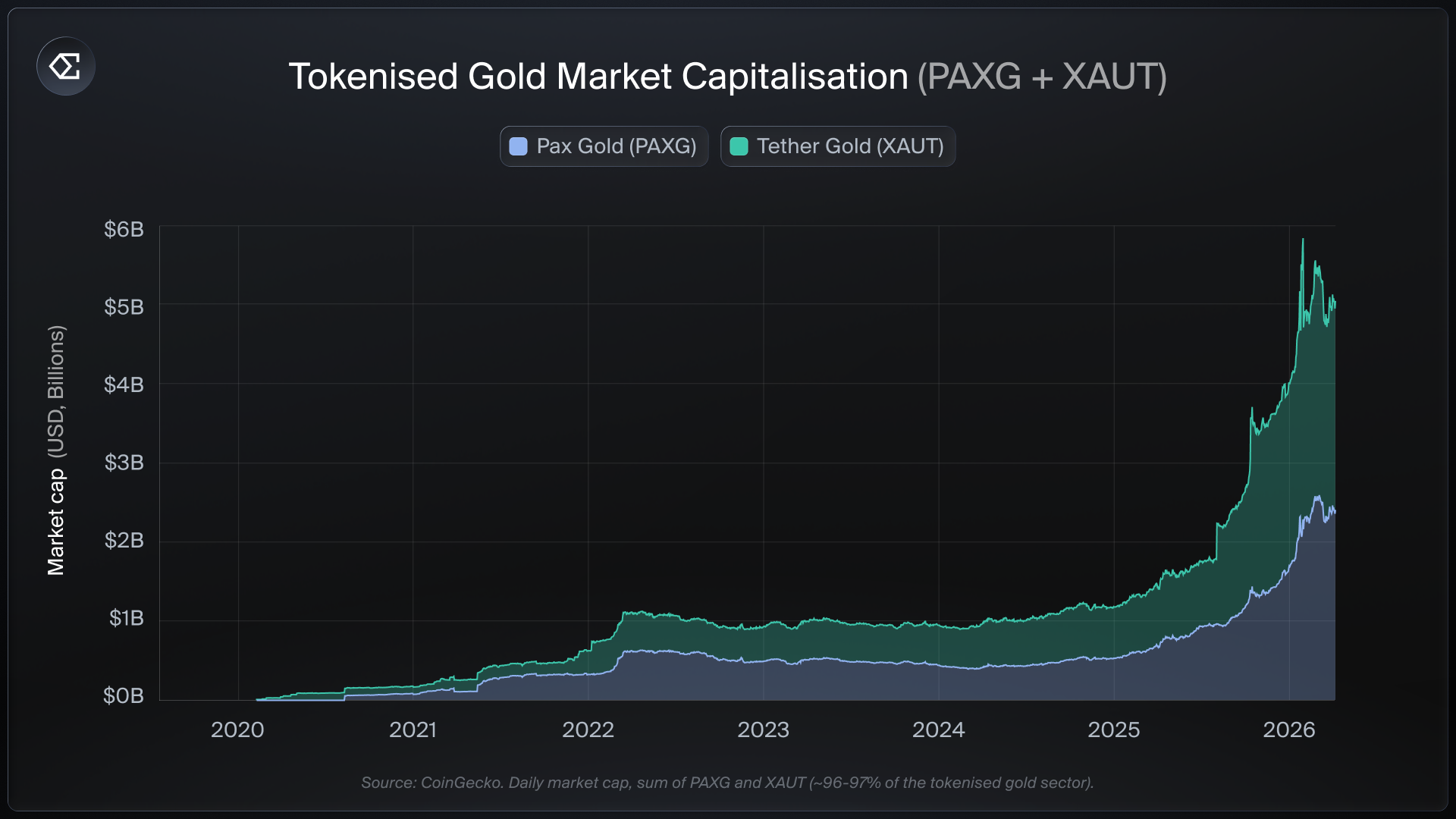

Gold Perpetuals Growth

Tokenised gold has grown from under $100M in combined market cap in 2020 to over $5B today. PAXG and XAUT dominate the sector and are two products with derivatives markets at institutional scale. The two assets track the gold price within a tight band in normal conditions, and are redeemable directly for physical gold or fiat via their respective issuers (Paxos for PAXG, Tether for XAUT).

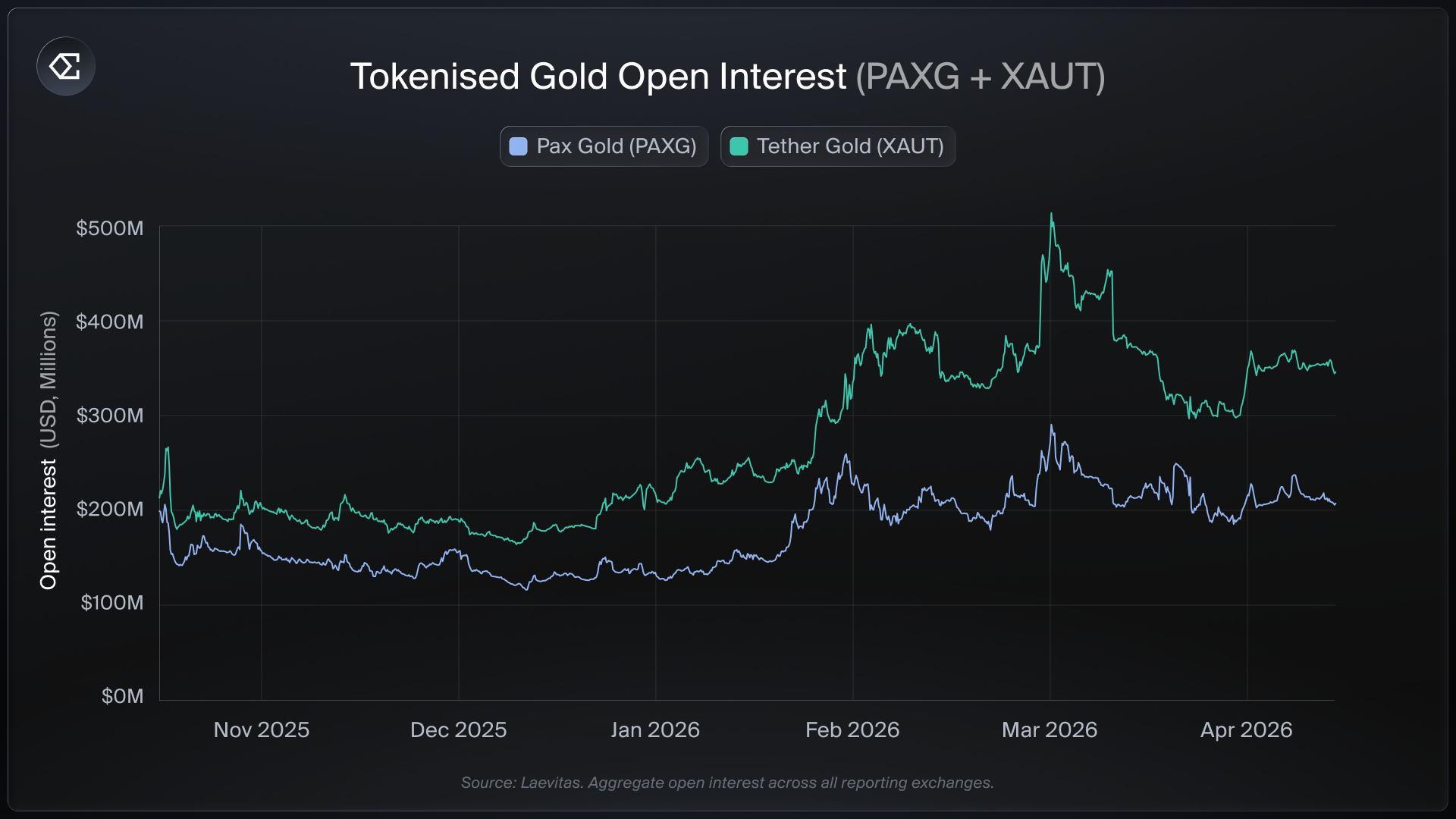

On the venues Ethena is already integrated with, aggregate open interest stood at $205M for PAXG and $293M for XAUT as of April. Binance is the dominant venue for PAXG at $159M in OI, while XAUT OI is led by Bybit and distributed across OKX, Bitget, and Binance.

Daily perpetual volume across Ethena exchanges has grown from under $200M in late 2025 to roughly $1B per day in recent weeks, with peaks approaching $2B during periods of elevated gold volatility.

Gold Funding Rates and Diversification of Returns

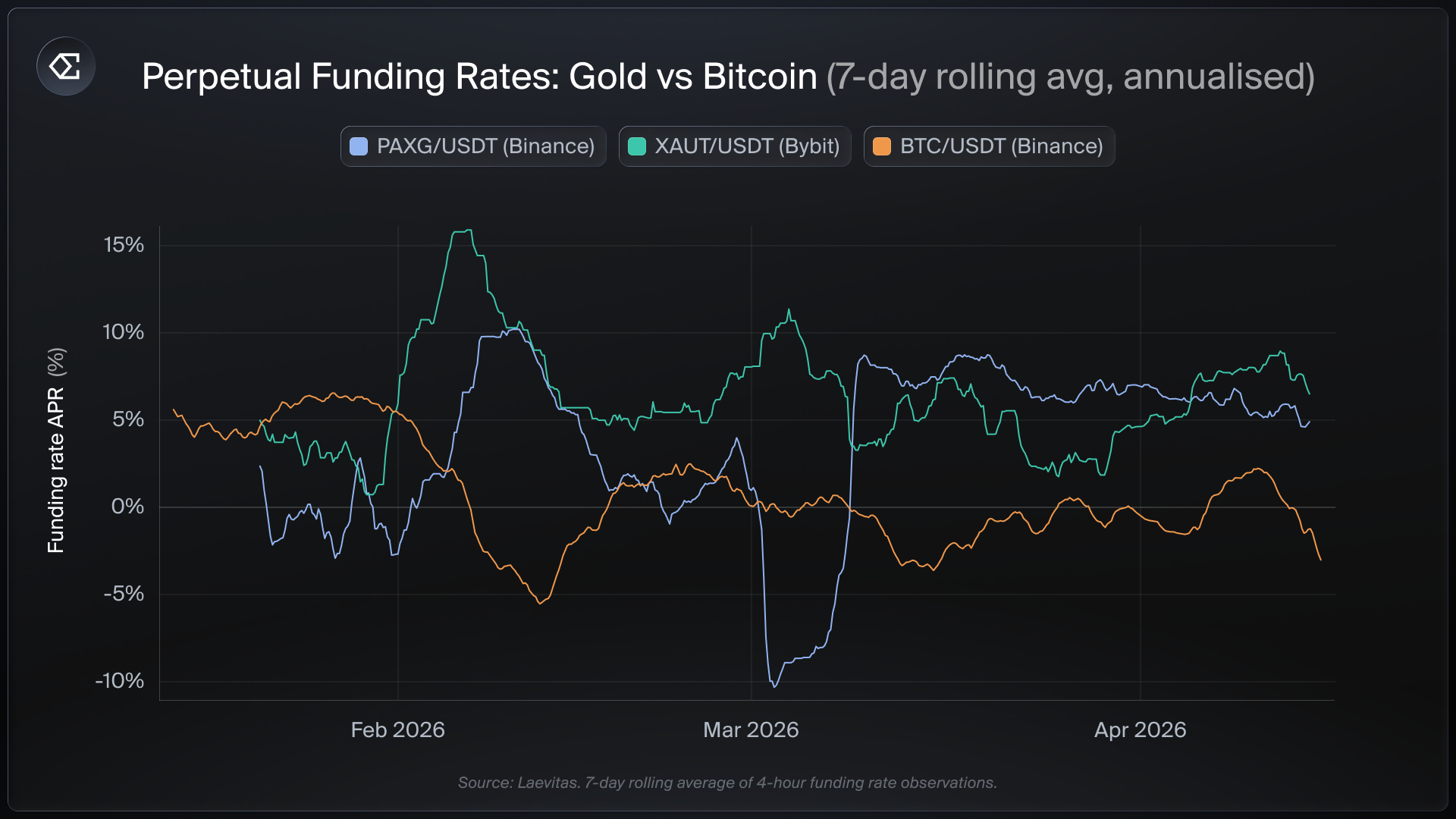

Funding rates on tokenised gold perpetuals have been consistently positive, reflecting persistent long-side demand from retail and institutional traders seeking leveraged gold exposure.

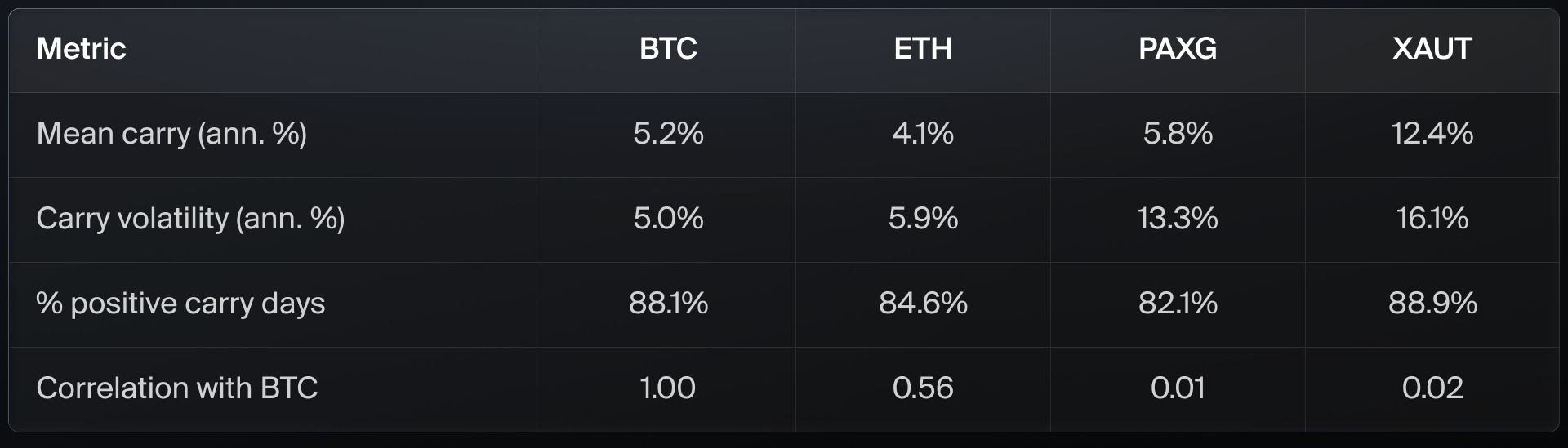

Over the past twelve months, mean annualised funding has been 5.8% for PAXG and 12.4% for XAUT, both comfortably above the 5.2% and 4.1% averages for BTC and ETH over the same window. Gold funding is more volatile day-to-day than crypto funding, a function of thinner markets, but is positive on 82-89% of days - in line with BTC (88%) and ETH (85%).

Higher funding rates alone is not the case for adding gold. The case rests on three properties that analysis by Blockworks Advisory has independently verified.

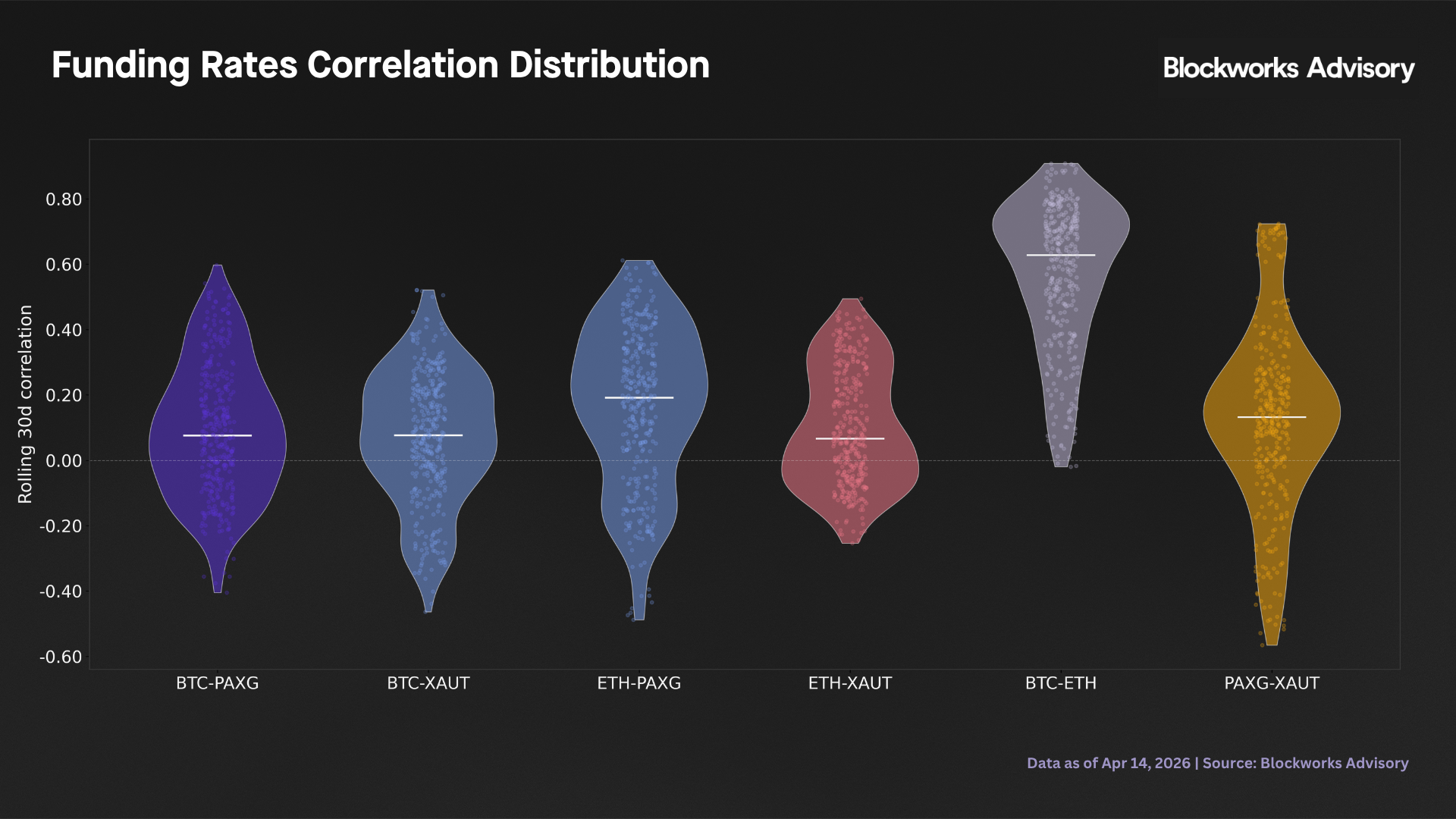

1. Gold and crypto funding rates are near uncorrelated.

Over the twelve-month sample, BTC-PAXG funding correlation is 0.01 and BTC-XAUT is 0.02. For reference, BTC-ETH correlation is 0.56. The two gold assets behave as though they were in a different asset class entirely from a funding-rate perspective, which provides diversification benefits for a basis trade portfolio just allocated to crypto perpetuals.

2. Gold funding tends to hold or rise when crypto funding compresses.

Blockworks applied a regime classification to BTC funding and split the sample into a “high funding” regime (61% of days, BTC carry ~7.5% annualised) and a “compressed carry” regime (39% of days, BTC carry ~1.4%). During compressed BTC regimes - the environment where sUSDe APY is most at risk - XAUT funding averaged 12.3% (vs. 9.0% in the high regime) and PAXG averaged 6.8% (vs. 5.8%). According to the analysis, Gold funding is directionally counter-cyclical to crypto funding, with the effect strongest in the low rate regime where diversification matters most.

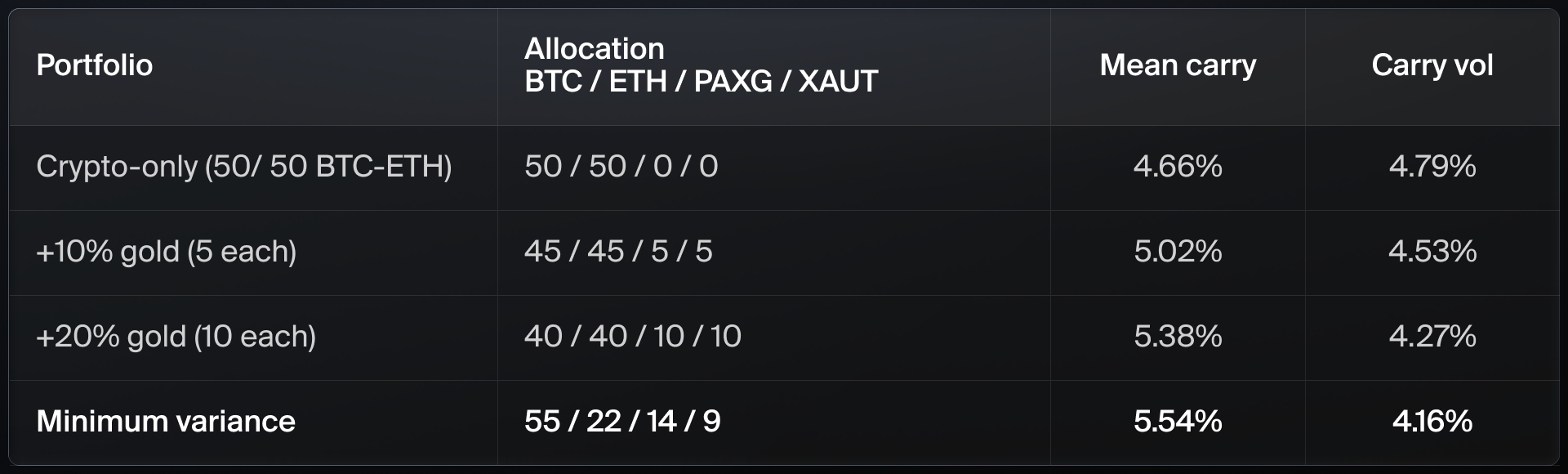

3. The addition of gold basis lifts carry and cuts volatility.

Adding a modest gold allocation to a crypto basis book raises mean carry and reduces carry volatility at the same time, rather than trading one for the other.

The Blockworks minimum-variance portfolio - the optimal allocation across all four assets based on correlations - sits at roughly 23% total gold weight (14% PAXG, 9% XAUT) and delivers 88 basis points of additional mean carry against a 13% reduction in rate volatility relative to a 50/50 BTC/ETH portfolio.

Separately, gold funding has proven resilient to gold’s own price moves. During the >25% gold drawdown in early 2026, XAUT perpetual funding on Bybit held in the high single digits rather than compressing.

An important caveat is that the twelve-month sample covers a single macro shift - specifically, a gold bull market followed by a correction - and does not include a sustained gold bear market. Gold perpetuals are nascent and have not experienced a sustained bear market regime. The correlation and return findings for gold perpetuals should be read as strong but will be updated as market history deepens.

The initial gold position sizes under consideration will be well below the $200M OI thresholds on PAXG and XAUT, consistent with the framework’s 10% max-position-to-OI cap, and will be scaled only as market depth and history support it.

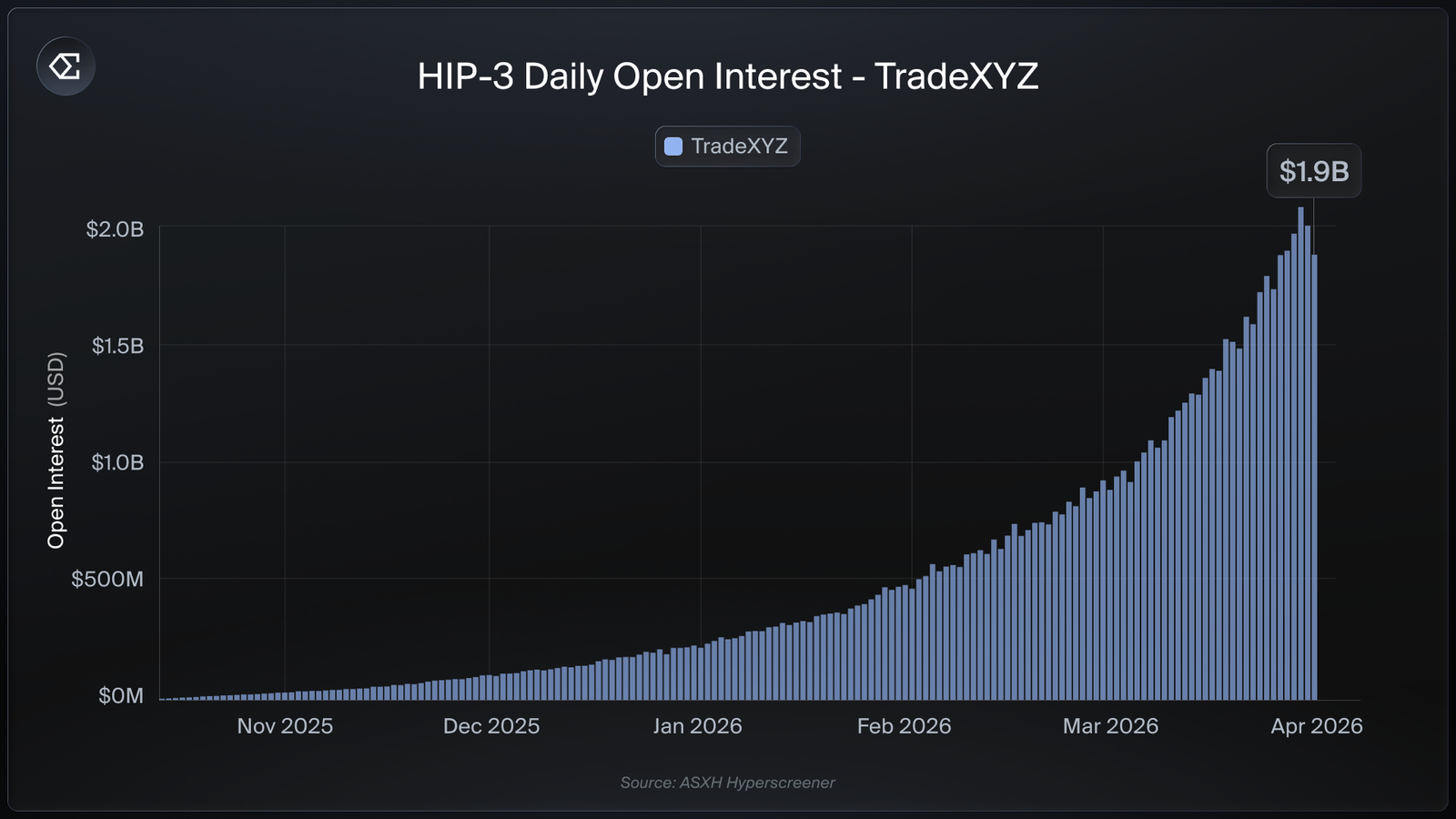

Looking Ahead: HIP-3 and Onchain Commodity/Equity Basis

The most significant development in the commodity and equity perpetual market over the past six months has been Hyperliquid’s HIP-3 framework, which enables permissionless deployment of perpetual futures for any asset with a reliable price feed. Since launching in October 2025, HIP-3 has grown from $70M in total open interest to close to $2B, and equity and commodity pairs now dominate the top of the market by OI.

For Ethena, HIP-3 represents a natural opportunity: the same delta-neutral methodology Ethena already runs at scale can be applied to a much broader set of underlying assets.

However, certain conditions apply before any HIP-3 market becomes eligible to be accessed for USDe’s backing strategy, and the Risk Committee will need to review any potential markets for feasibility.

Hyperliquid is not currently on Ethena’s approved list of hedging venues for USDe backing. Onboarding an onchain venue introduces considerations that are distinct from centralised exchanges, including smart contract risk, oracle design, and different ADL mechanisms.

Adjusting the Framework for Commodities

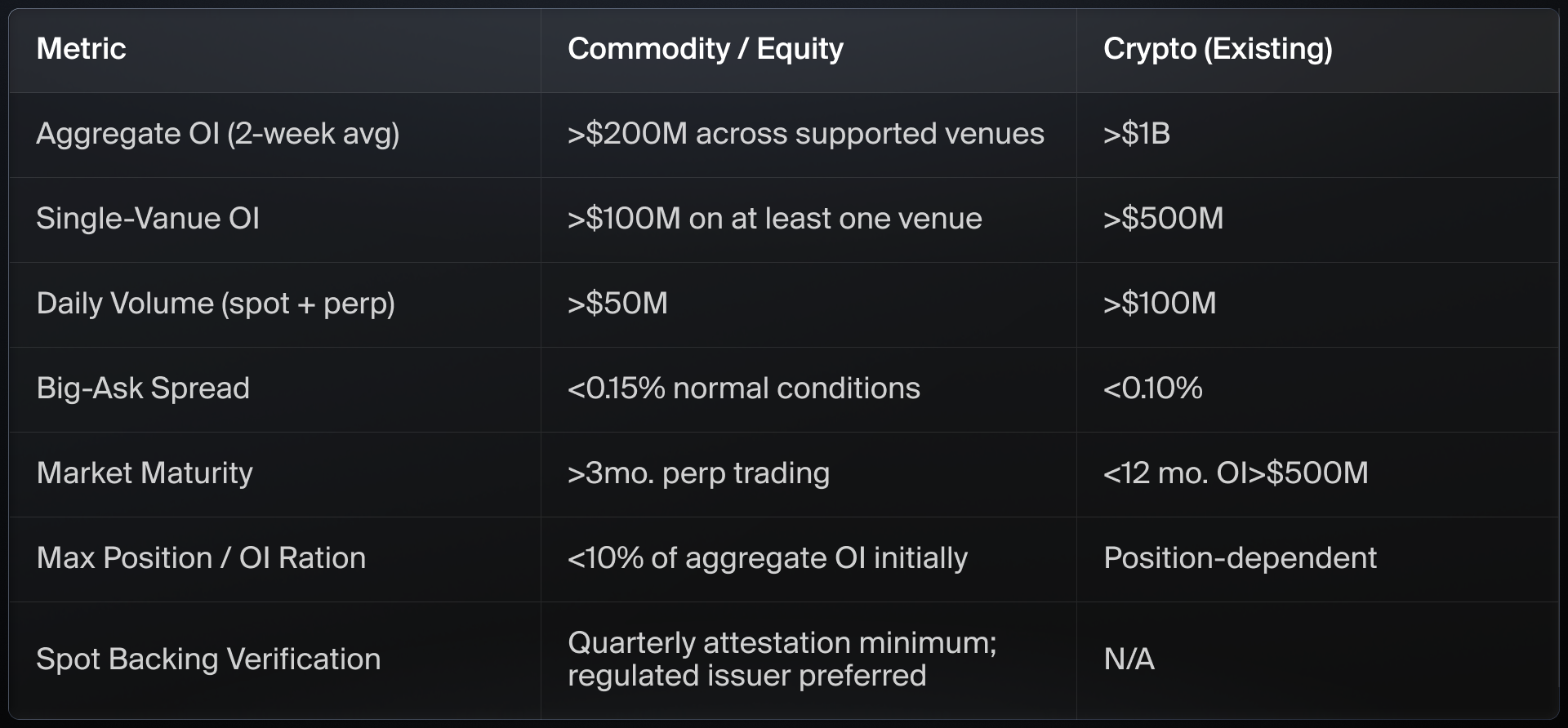

The existing Eligible Asset Framework for USDe, published in August 2025, was built for crypto-native assets. It set a $1B aggregate open interest (OI) threshold across supported venues, a $500M single-venue minimum, and related parameters for liquidity, spread, and market maturity. Those thresholds reflect the volatility and market structure of BTC, ETH, and other crypto assets.

Gold and other commodity perpetuals have a different risk profile:

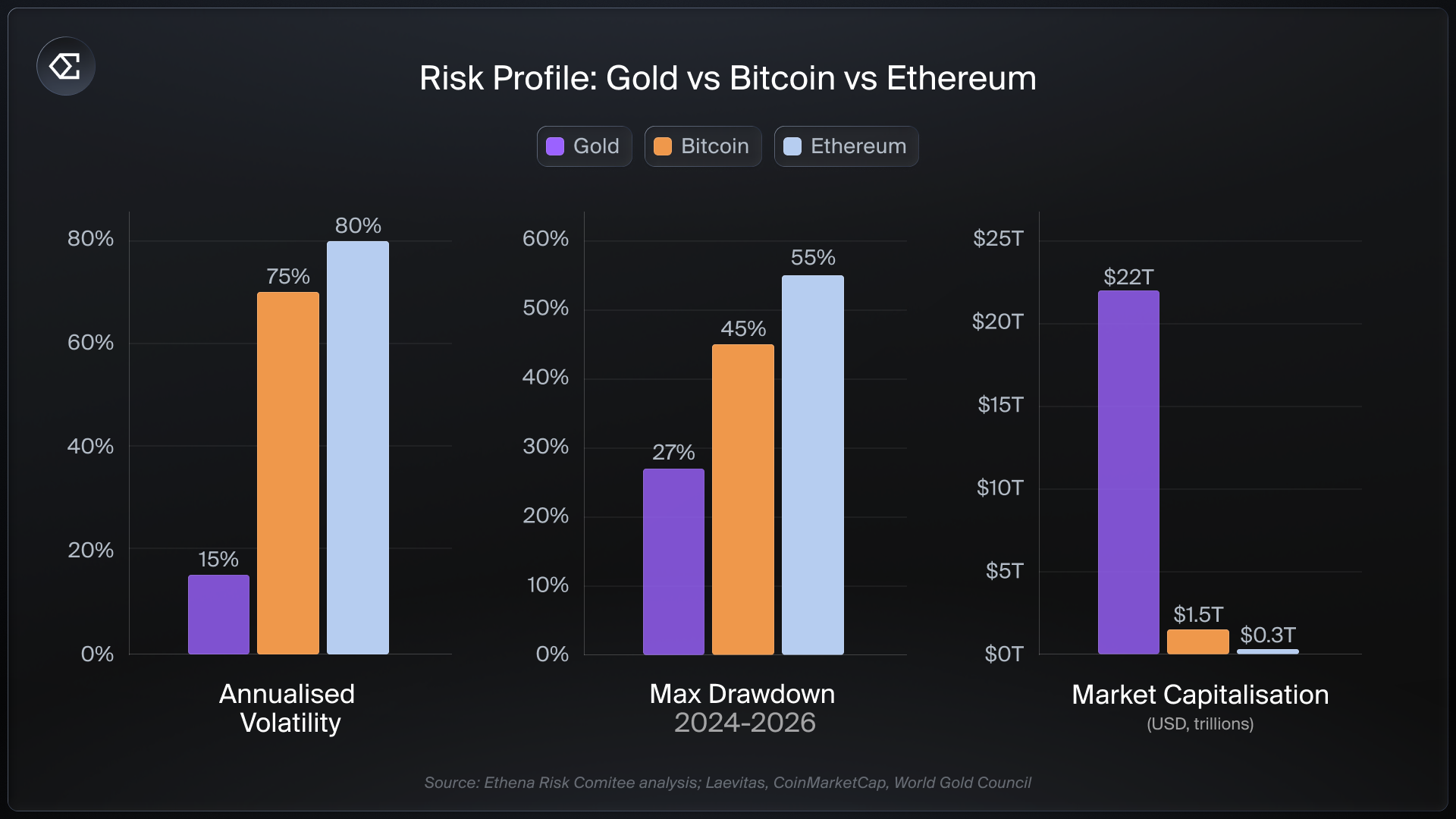

- Lower underlying volatility. Gold’s annualised volatility is approximately 15%, roughly 4-5x lower than BTC (~60-80%) and 5x lower than ETH (~70-90%) over the last 5 years. Over the last 12 months, Gold’s volatility was 25% vs BTC 43% and ETH 71%. At equal notional, a gold position carries meaningfully less risk than a crypto position.

- Diversified structural demand. Central banks purchased over 4,000 tonnes of gold from 2022-2025. Gold ETFs absorbed $89B of net inflows in 2025 alone, while electronics absorbed roughly $30B of gold in 2025. In Q1 2026, the World Gold Council said “global AI infrastructure deployment continued to support industrial gold demand.” These demand drivers are largely independent of crypto market cycles.

A $1B OI threshold designed for crypto markets would preclude every commodity perpetual today, despite the commodity asset class being more mature and less volatile. The adjusted framework approved by the Risk Committee introduces new thresholds for commodity perpetuals accordingly:

Equity perpetuals will follow a similar framework and analysis will be posted separately.

The $200M aggregate OI threshold reflects gold’s volatility relative to crypto: at 15% volatility versus ~70% for crypto, $200M in gold OI provides equivalent risk capacity to approximately $930M in BTC or ETH OI.

The framework also adds constraints specific to commodity and equity markets: a preference for regulated issuers with independent attestation of the spot backing, direct fiat or physical redemption as a backstop on the spot leg, and a ceiling on round-trip fees to ensure the basis trade remains economic at scale.

Ethena’s Basis Strategy Going Forward

The commodity basis allocation will sit alongside the existing USDe backing, sized within caps set by the Risk Committee and subject to the same ongoing monitoring applied to every other position. The crypto basis trade remains a core pillar of USDe’s backing.

The Risk Committee’s assessment of tokenised gold products, along with the recalibrated commodity framework, is published on the Ethena governance forum. As with every prior extension of the backing, Ethena will continue to operate within a defined, publicly disclosed risk framework so that the community can evaluate the guardrails and hold us accountable to them.

The original commodity framework analysis by Kairos Research can be viewed here.

The extended Blockworks analysis on Gold perpetuals can be viewed here.