USDe RWA Backing Diversification: Extending Beyond Treasuries

This post is a continuation of our earlier piece on USDe backing diversification, focusing on the next phase of that work: broadening real-world asset (RWA) exposure beyond tokenised T-Bills.

USDe’s backing already includes meaningful indirect RWA exposure through USDtb - a stablecoin backed primarily by BlackRock’s BUIDL, that has provided a useful diversification tool when crypto rates aren't attractive.

The next step is to broaden RWA holdings into additional categories of high-quality fixed income, subject to a defined risk framework set by the Ethena Risk Committee. Asset categories under evaluation are subject to strict criteria, including but not limited to:

- Credit Quality

- Drawdown profile

- Liquidity

- Pricing

There are categories this framework deliberately excludes. Private credit, long-duration fixed income, and any asset class without strong liquidity at NAV are not eligible assets for reasons outlined below.

Why RWAs Demand a Stricter Risk Framework

The basis trade at the core of USDe’s backing architecture is delta-neutral by design. A 10% drawdown in spot collateral is offset by a 10% gain on the short hedge. Funding risk, custodial risk, and execution risk all exist, but directional drawdown risk in the spot asset itself does not flow through to USDe’s backing in most market conditions. With regards to RWAs, there are more risk considerations to account for:

Four constraints define the eligible RWA assets:

- Credit quality. Only the highest tranches of the capital stack, with deep historical performance data across prior stress windows including the Global Financial Crisis, COVID-19, and the 2022 rate cycle.

- Drawdown profile. Both peak-to-trough magnitude and recovery time, evaluated against the size of the Reserve Fund and the redemption capacity USDe needs to support.

- Liquidity. Strong liquidity at NAV with close to daily settlement, deep secondary markets, and demonstrated ability to absorb institutional-size flow without meaningful price impact.

- Pricing transparency. Independent third-party pricing, daily NAV publication by an independent administrator, and no reliance on internal marks or appraisals.

Private credit falls outside this framework on liquidity and pricing transparency grounds. Long-duration investment-grade credit falls outside on drawdown profile - a long duration investment-grade bond portfolio took a roughly 22.7% drawdown in 2022 as rates moved, which is too much risk per unit of return to make sense for USDe’s backing.

AAA CLOs as the Starting Point

The first asset category under active evaluation is AAA-rated collateralised loan obligations, specifically the Janus Henderson Anemoy AAA CLO Fund - a BVI-domiciled tokenised fund issued via Centrifuge with Janus Henderson Investors US LLC as sub-investment manager, running the same portfolio team and the same AAA CLO mandate as the Janus Henderson AAA CLO ETF (JAAA).

LlamaRisk, a member of the Ethena Risk Committee, has conducted independent due diligence on JAAA and approved it as a USDe backing asset.

Asset class profile

AAA CLOs sit at the top of the CLO capital stack. The underlying tranches are floating-rate, supported by structural subordination from the mezzanine, BBB, BB, and equity tranches that absorb losses before the AAA. The asset class has a zero default rate at the AAA level across the entire history of modern CLO issuance, spanning the Global Financial Crisis, the 2015–16 energy shock, COVID-19, and the 2022 rate-and-spread cycle.

The U.S. AAA CLO market is one of the most liquid in finance, sitting at approximately $500–$600 billion outstanding across 3,000+ AAA-rated tranches managed by 135+ CLO managers. AAA tranches accounted for 54% of 2025 U.S. CLO new issuance by original face value. The tranche universe and the manager universe are deep and diversified.

The JAAA ETF - the longer-track-record liquid version of the same strategy - carried $27.17 billion in net assets across 610 positions as of May 2026, and is the largest fixed-income ETF launched in the last five years. The Centrifuge-tokenised fund reached approximately $1.1 billion at peak in early 2026 and currently sits at roughly $412 million across seven supported chains. Janus Henderson Investors as a firm manages approximately $373 billion in total assets.

Drawdown profile

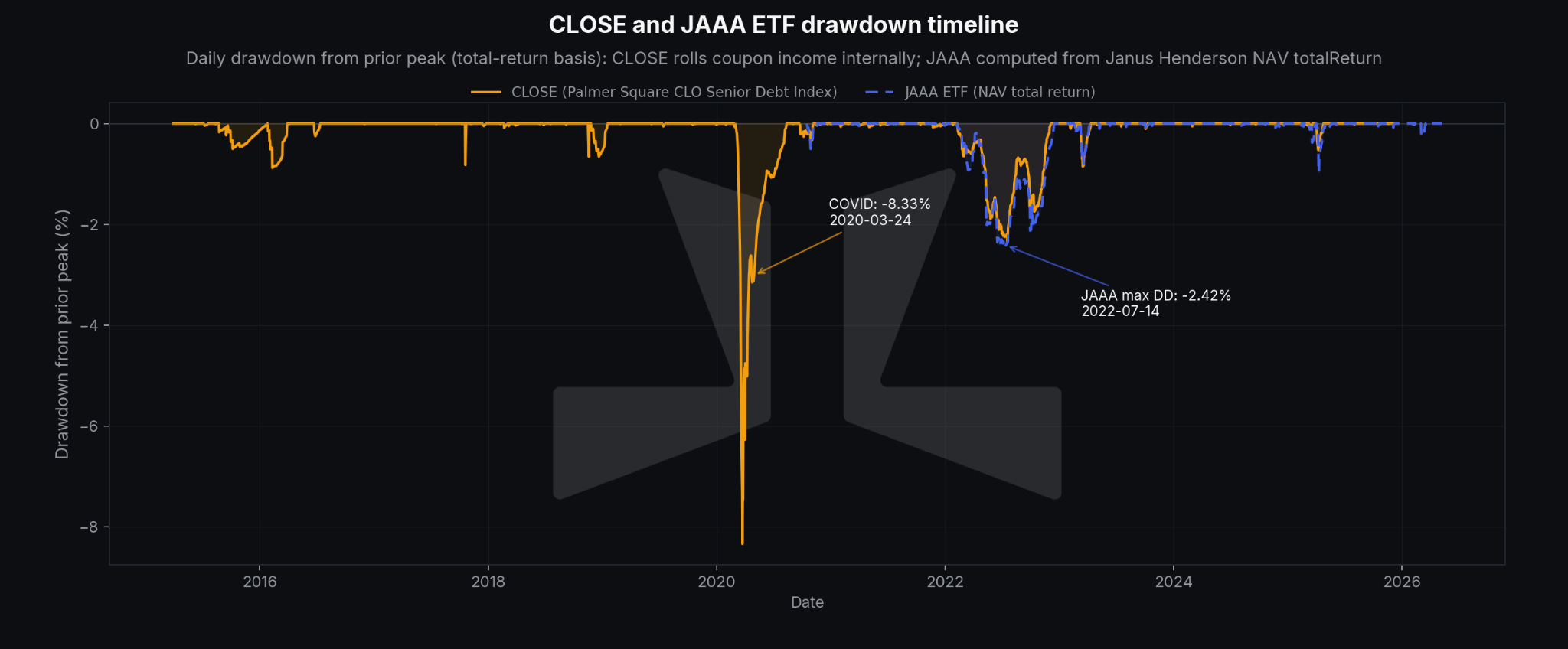

The JAAA ETF has been live since October 2020. Across 1,395 trading days through 2026-05-08, the worst single-day NAV move was –0.60% on 2022-05-12, and the maximum peak-to-trough drawdown was –2.42%, with the trough on 2022-07-14, during the Fed rate-hiking cycle. Daily returns show a tight distribution: median +1.98 bps, standard deviation 5.98 bps, with 8.6% of days posting a negative return.

JAAA’s inception postdates COVID-19, so its time series does not contain a true tail event. To extend the stress window, LlamaRisk uses the Palmer Square CLO Senior Debt Index (CLOSE), which tracks the same senior AAA segment of the broadly-syndicated CLO market and publishes a daily total-return series since 2015. The 7-day return correlation between JAAA NAV and CLOSE over the overlap window is 0.86, with a beta of 0.95 - a defensible long-history proxy for stress analysis.

On CLOSE, the COVID-19 liquidity crisis produced a –8.33% peak-to-trough drawdown (peak 2020-02-26, trough 2020-03-24), recovered to peak by 2020-08-12. That is the binding tail observation in the available history, and the appropriate stress reference point for sizing the position.

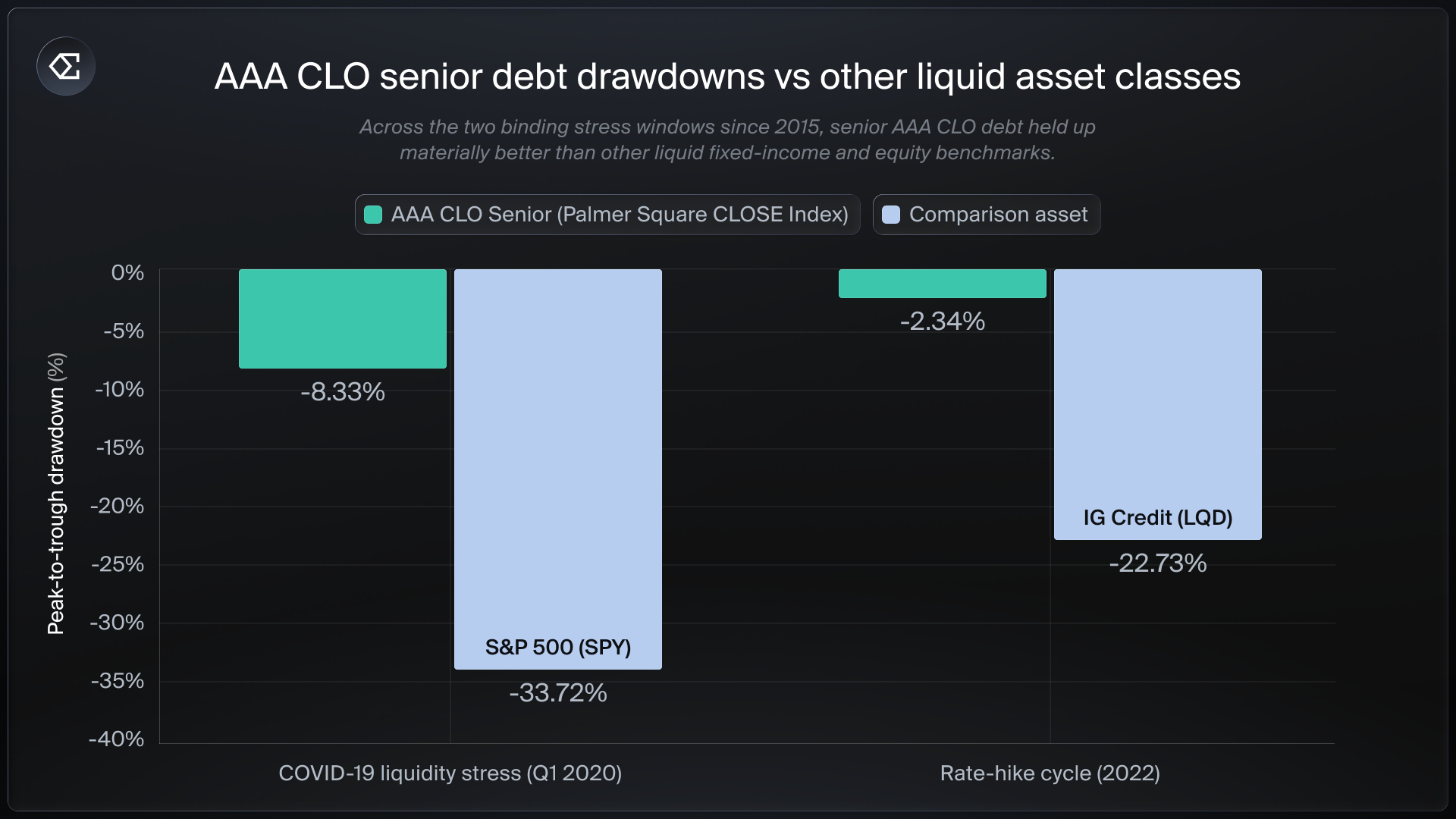

Source: LlamaRisk JAAA Asset Onboarding analysis (2026-05-12). Comparison assets: SPY (S&P 500 ETF), LQD (iShares iBoxx $ Investment Grade Corporate Bond ETF).

Two points stand out from this comparison. First, AAA CLO senior debt drew down by less than a quarter of what the S&P 500 lost during COVID-19, and by roughly a tenth of what investment-grade corporate credit lost during the 2022 rate cycle. Second, the COVID episode is the only meaningful stress in 11 years of CLOSE daily history - the asset class spends almost all of its time within a tight band around zero drawdown.

Stress duration

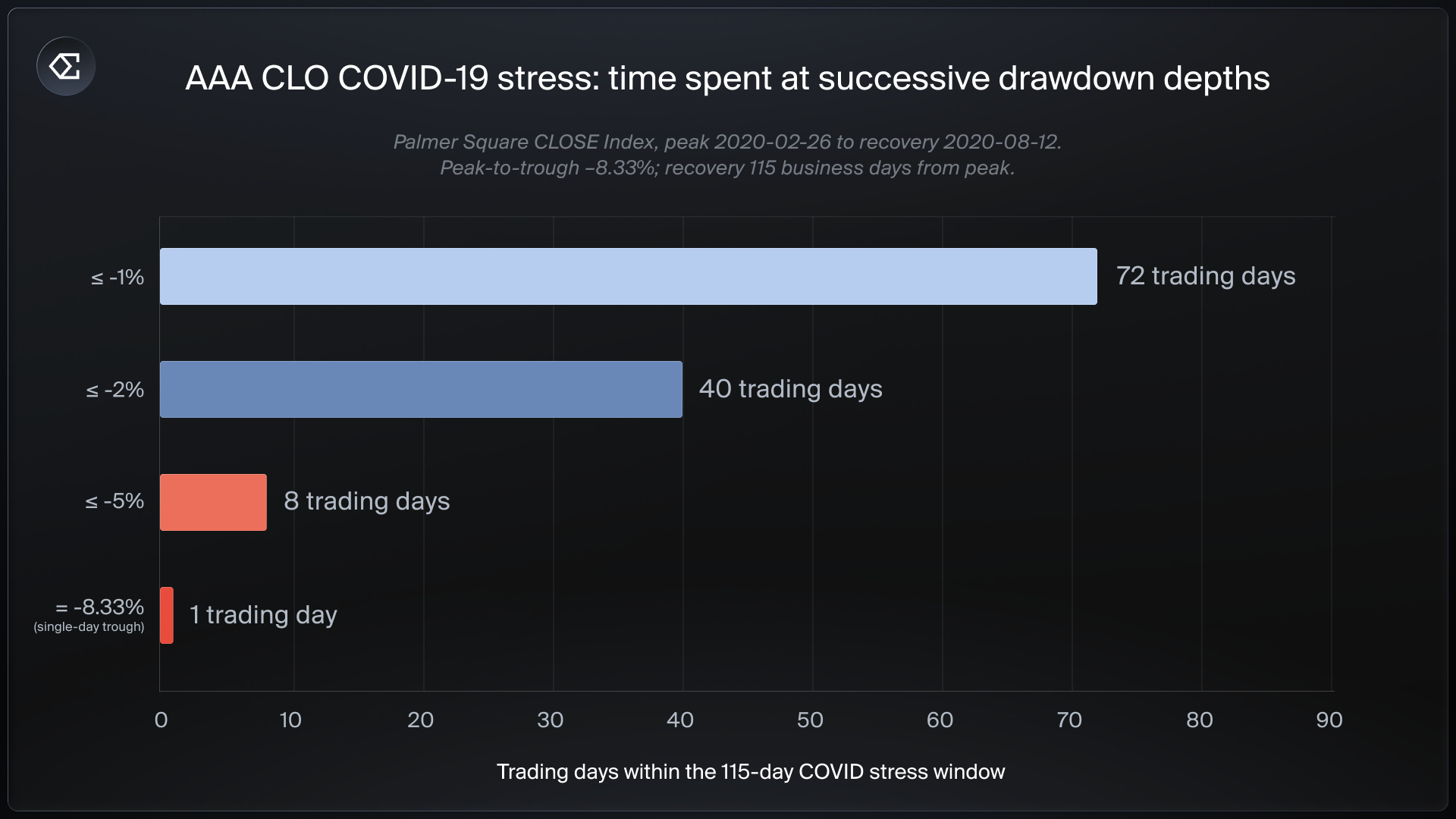

Drawdown depth is one dimension; time to recover is another. The COVID episode took 19 business days to fall from peak to trough and 115 business days from peak to full recovery. Within that 115-day window, CLOSE held at successively deeper drawdown depths for the following durations:

Source: LlamaRisk JAAA Asset Onboarding analysis (2026-05-12), Palmer Square CLOSE Index.

The interpretation is that even in the tail scenario observed over the last decade, the AAA CLO position spent only eight trading days at –5% or deeper, a single day at the –8.33% trough, and the remainder recovering. The shape is short and shallow relative to the equity and IG credit comparisons.

Centrifuge fund vs ETF: how comparable are they?

Statistics from the ETF’s longer track record (and from CLOSE’s longer-still history) are only useful if the Centrifuge-tokenised fund holds a comparable portfolio. LlamaRisk’s due diligence addresses this on four dimensions:

- CUSIP overlap. Twelve of the Centrifuge fund’s twenty CLO positions - 60.42% of fund weight - match CUSIPs in the ETF’s 551-line holdings file. A CUSIP is a nine-character code that uniquely identifies a North American financial security. All eight non-matching positions are managed by issuers also present in the ETF; the divergence is at tranche level, within the same issuer set.

- Manager concentration. The Centrifuge fund is more concentrated than the ETF - 47.2% in the top three managers vs 13.0% in the ETF - reflecting its smaller size ($412M vs $27.17B). All Centrifuge managers are also approved managers in the ETF, so the concentration is in tranche selection within the same vetted pool, not in new issuers.

- Vintage. The Centrifuge fund weights toward 2017–2022 vintages (77.5% cumulatively), while the ETF skews more recent (2023–2025 at 42.5%). All twenty Centrifuge positions are senior AAA tranches with floating-rate coupons, consistent with the mandate floor of 80% AAA maintained.

- Realised co-movement. Over 198 daily observations from Centrifuge inception (2025-07-28) to 2026-05-08, the Centrifuge token returned 4.40% annualised against the ETF’s 5.06% - a 67 bps gap, consistent with the 20 bps headline management-fee differential plus additional pass-through service-provider fees on the Centrifuge wrapper. Seven-day return correlation is 0.74.

LlamaRisk’s conclusion is that ETF-derived stress metrics, and CLOSE-derived long-history stress metrics, are a defensible lower bound on Centrifuge specific risk - market-wide stress events are correlated with similar impact, while concentration differences are handled separately through the allocation cap and the response framework below.

Sizing the Allocation and Responding to Stress

The diligence above sets the asset-class profile. Two further pieces of the framework convert that profile into operational constraints: an explicit allocation cap derived from a Reserve Fund stress-loss budget, and a defined response mechanism if a held position moves into drawdown.

Allocation cap from a stress-loss budget

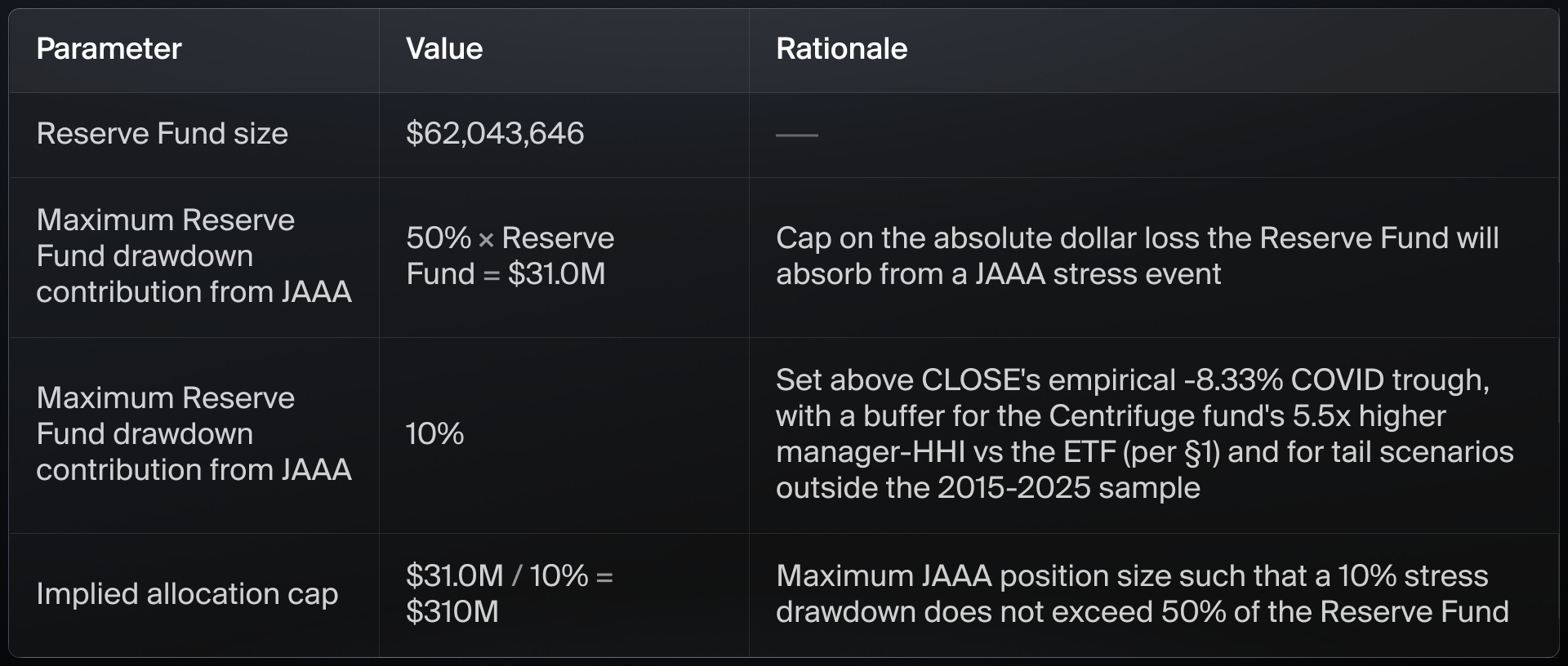

LlamaRisk’s recommendation, which the Risk Committee will use as the basis for sizing, builds the cap from three inputs:

- Reserve Fund coverage. No single new position should implicate more than 50% of the Reserve Fund in stress test estimates below. The remaining 50% of Reserve Fund headroom is preserved for stress contributions from other risk-bearing positions Ethena holds.

- Stress assumption. A 10% peak-to-trough loss assumption is applied to the JAAA position. This sits above CLOSE’s empirical -8.33% COVID trough, with a buffer for the Centrifuge fund’s higher manager concentration relative to the ETF and for tail scenarios outside the 2015-2025 sample.

- Implied cap. At a Reserve Fund size of approximately $62 million as of the diligence date, a 10% stress assumption against a 50% Reserve Fund contribution implies a maximum JAAA position size of approximately $310 million.

Diversification Within the RWA Sleeve

No single RWA position will dominate the backing. The criteria caps individual positions and individual issuers within the broader RWA sleeve, and the Risk Committee monitors both concentration limits and rolling drawdown on an ongoing basis.

The diversification principle applies inside the RWA category as well: spreading exposure across multiple high-quality credit products and issuers produces a more resilient sleeve than any single allocation. Future allocations may extend the sleeve into the other categories listed above, once independently assessed by the Risk Committee against the framework described in this post.

What This Means for USDe

The returns on the perpetual futures basis trade are correlated with the crypto market cycle. When funding is high, basis returns are strong; when funding compresses or turns negative, returns soften. That cyclicality is a feature of the trade the protocol has run since launch.

RWA exposure breaks that correlation. AAA CLO yields are driven by short-rate policy, credit-spread dynamics, and loan market structure - none of which are tied to crypto positioning or sentiment. The floating-rate structure of the underlying tranches means the position carries effectively no duration risk, with an effective duration of approximately 0.20 years.

Adding a meaningful, well-sized RWA sleeve to USDe’s backing produces a portfolio whose returns are more stable across market environments, and whose tail risk is diversified across independent drivers.

The result is a set of assets that earns competitively in any market environment, with a backing composition whose performance does not depend on any single source of return continuing to deliver.

All RWA allocations are independently assessed and formally approved by the Ethena Risk Committee. LlamaRisk’s full JAAA Asset Onboarding analysis, together with the Risk Committee’s deliberations, will be published on the Ethena governance forum.

Reporting and attestation infrastructure will scale with the backing’s composition, with Proof of Reserves remaining unchanged and additional reporting initiatives to follow.

If you have questions on any of these initiatives, we would be happy to provide further information.