USDe Backing Diversification: Building Resilience Across Market Cycles

The backing of USDe has historically been primarily composed of short perpetual futures positions against spot crypto collateral, generating returns through funding rate collection. However, perpetual futures positions make up just 11% of the USDe backing today, with the rest allocated to a variety of stablecoin reserve and DeFi lending positions.

Any portfolio concentrated in any single strategy carries inherent risk. While the historical framework for USDe has not resulted in any impairments of the backing, utilisation of the Reserve Fund, or critical issues, we are proactively diversifying the composition of USDe’s backing to reduce concentration risk and build a more resilient reserve portfolio - one designed to perform across all market environments, including periods where crypto-native funding rates compress.

This backing diversification includes four areas, each of which represents a natural extension of what Ethena already does today:

- Overcollateralised institutional lending of stablecoins, utilising third-party institutional custodians to custody the borrower’s collateral assets

- Real-world assets (RWAs) beyond T-Bills, broadening into additional high-quality liquid credit products

- Equity and commodity basis trades, extending the same delta-neutral methodology Ethena already applies to crypto assets

- Prime Lending to trading firms via overcollateralized loans, with exchange risk taken on by the counterparty.

Each of these strategies is additive and sized conservatively, with the basis trade remaining a core pillar of USDe’s backing when the market environment is suitable. The product’s fundamental architecture and redemption mechanism are unchanged.

All of these initiatives have been, or will be, independently assessed and approved by the Ethena Risk Committee, which sets allocation caps, counterparty standards, collateralisation requirements, and liquidity coverage parameters, and monitors positions on an ongoing basis. Testing for some of these initiatives is underway and we expect certain strategies to go live shortly, if approved.

Overcollateralised Institutional Lending

We are in the process of finalising our first direct lending agreements via Anchorage Digital, Maple Institutional, and Coinbase Asset Management, among others. These agreements contemplate Ethena lending stablecoins from the USDe backing to facilitate overcollateralised lending originated by the entities mentioned above held in secured triparty custody.

These loans operate within defined parameters provided by the Ethena Risk Committee, including minimum overcollateralisation ratios, concentration limits, and liquidity requirements. Each loan is overcollateralised with defined margin call and automatic liquidation ratios, and has tenors designed to minimise liquidity risk for large USDe redemption scenarios.

Ethena already lends stablecoins from the backing of USDe into DeFi markets such as Aave and Morpho. This represents a natural extension of that existing activity - overcollateralised lending with only high-quality, immediately liquid collateral (BTC/ETH) and facing institutional counterparties that meet strict eligibility criteria.

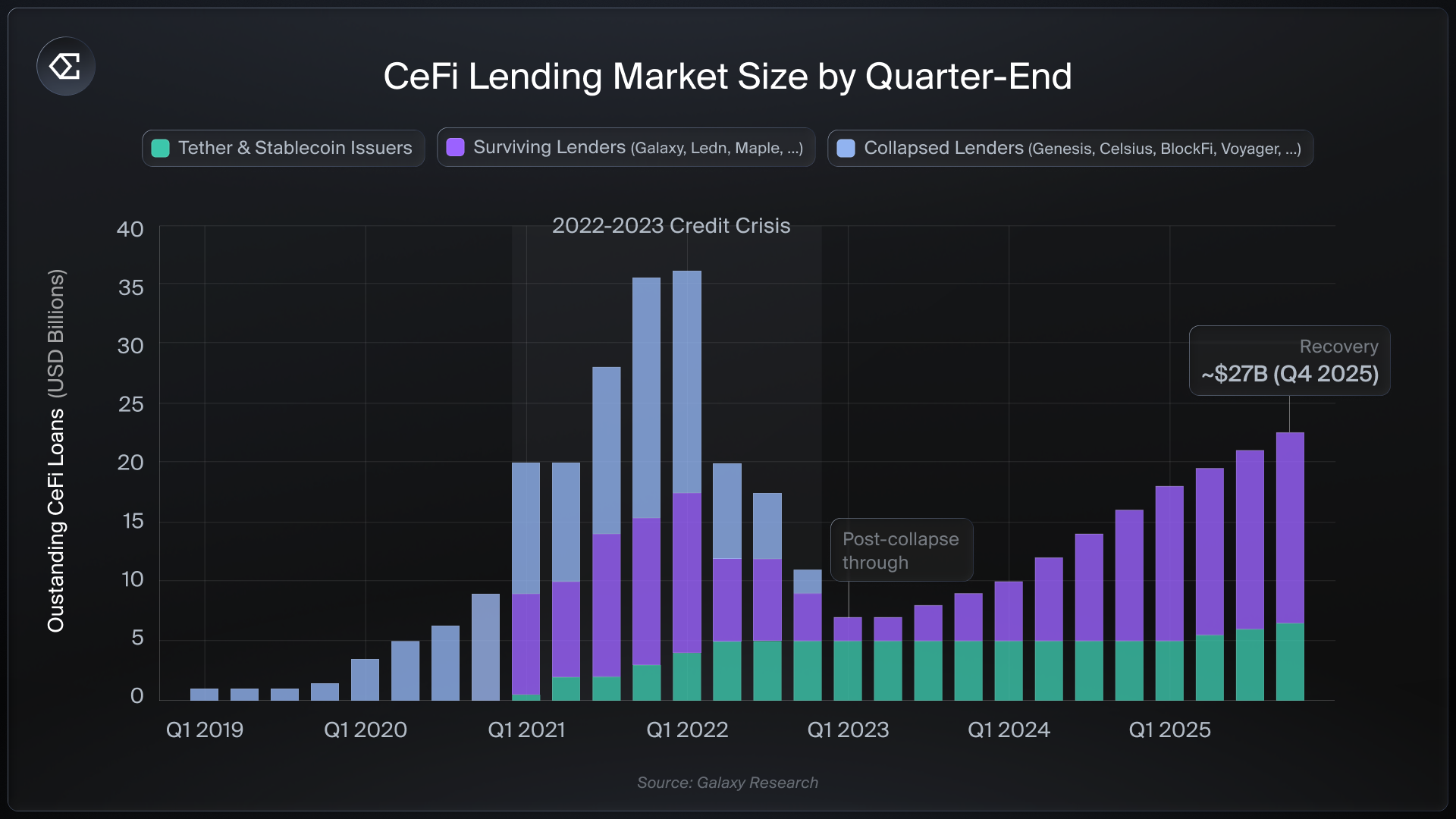

The Institutional Lending Market Today

The CeFi lending market has undergone a structural reset since the credit crisis of 2022–23, where failures of undercollateralised lenders like Genesis, Celsius, and BlockFi eroded trust across the industry. Since then, the market has recovered on a fundamentally different footing: overcollateralised, transparent, and with rigorous counterparty standards.

CeFi Lending Market Size by Quarter-End. Source: Galaxy Research.

Crypto-collateralised lending reached an all-time high of $73.6B in Q3 2025, with the composition of that leverage structurally healthier than during the previous cycle. Overcollateralised credit and transparent reporting have become the norm. Ethena’s direct lending activity will sit firmly within this reformed landscape - facing only institutional counterparties, overcollateralised with high-quality liquid collateral, and subject to the independent oversight of the Risk Committee.

Prime Lending

Ethena is also exploring, pending Risk Committee approval, further secured lending with participants trading on different exchanges requiring different margin & settlement currencies than what they presently hold. With these loans, Ethena would not be taking any exchange risk or incremental counterparty risk to the trading firm in the event of losses given they have overcollateralized the loan with assets held by a third-party custodian with clear margin and liquidation thresholds.

Real-World Assets

Ethena has already allocated to RWAs via tokenised T-Bills and adjacent assets, primarily through our USDtb product - a stablecoin backed by BlackRock’s BUIDL, where Ethena receives distributions of revenue from USDtb’s reserves under a separate agreement.

The next phase of this backing diversification involves broadening reserve composition into additional asset categories, subject to strict credit quality, liquidity, and volatility criteria that will be defined by the Ethena Risk Committee. These may include, but are not limited to:

- Collateralised Loan Obligations (CLOs)

- Investment-grade corporate bond funds

- Diversified short-duration credit funds

- Structured credit products with strong liquidity

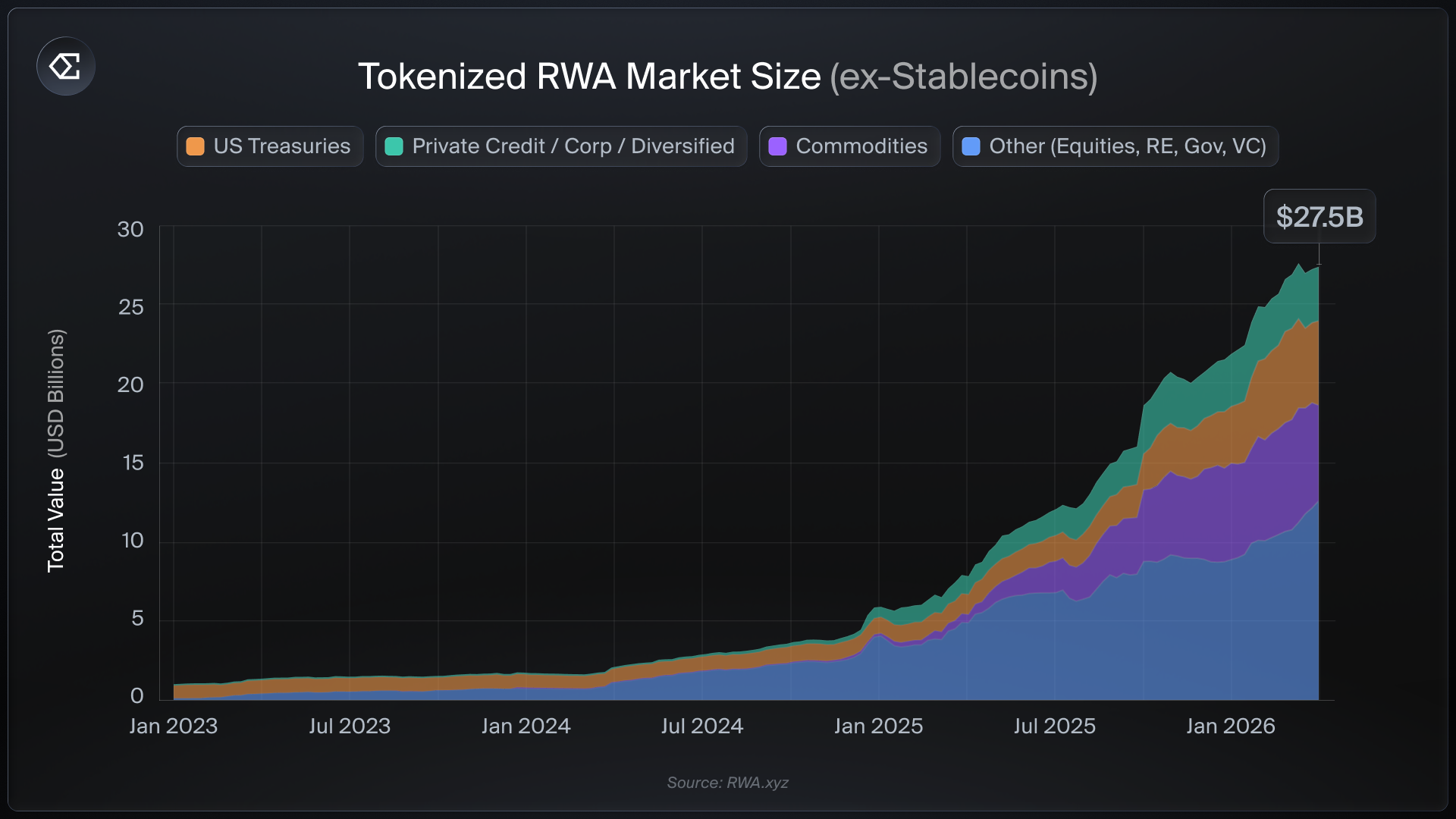

The Tokenised RWA Market

The market for tokenised real-world assets (excluding stablecoins) has grown nearly fivefold over the past two years, surpassing $26B in on-chain value. Six categories of tokenised assets have now passed the $1B mark: private credit, commodities, US Treasuries, corporate bonds, non-US government debt, and institutional alternative funds.

Tokenised RWA Market Size (ex-Stablecoins). Source: RWA.xyz

This growth reflects a broader trend of institutional adoption. BlackRock’s BUIDL fund, Apollo’s ACRED, and a range of tokenised credit and equity products from issuers like Securitize and Centrifuge have brought meaningful institutional-grade assets on-chain. Ethena intends to allocate into the highest-quality segments of this market, within defined parameters.

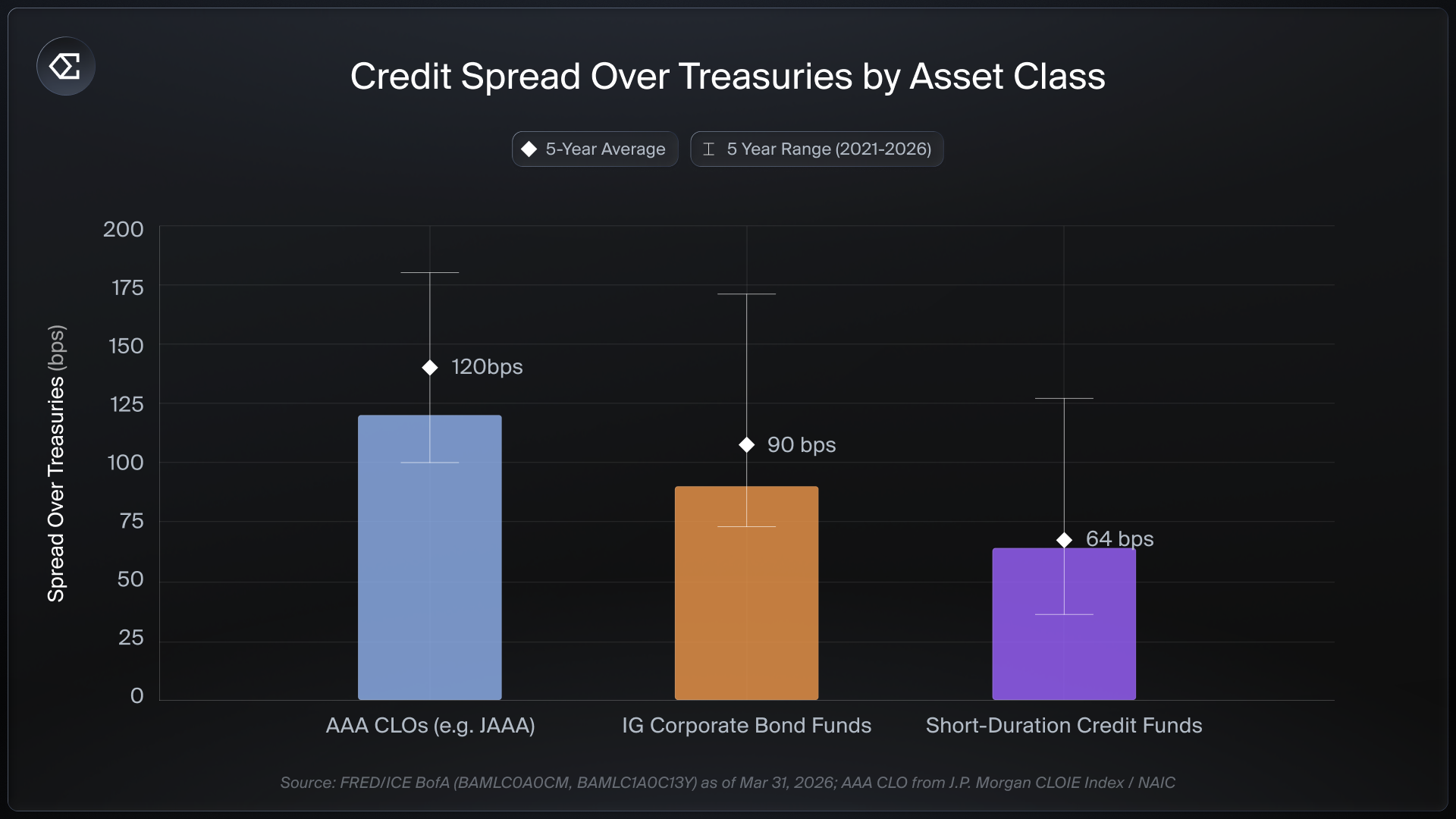

Credit Spreads Across Asset Classes

Ethena will take a disciplined and conservative approach to scaling into RWAs outside of T-Bills. Initially, allocations will likely be limited to AAA-rated CLO funds, which have had no history of defaults. The chart below provides context on the spread available across the asset classes under consideration, relative to T-Bills.

An example of an asset class Ethena may allocate to initially are AAA rated CLO's. AAA CLO's offer strong liquidity - a key requirement under the risk framework. They carry an AAA credit rating and provide modest additional spread over T-Bills while maintaining a strong liquidity and credit profile.

Any assets that don’t meet Ethena’s credit quality, volatility, or liquidity criteria will not be held in the backing of USDe. All allocations operate within defined parameters and allocation caps set by the Ethena Risk Committee, which independently assesses each asset before approval.

Equity and Commodity Basis Trades

Pending Risk Committee approval, Ethena is also planning to extend its existing basis trade framework into equity and commodity markets. This represents a natural extension of Ethena’s core competency - the same delta-neutral basis trade methodology applied to adjacent markets where sufficient open interest now exists.

Ethena has operated one of the largest delta-neutral books in the industry for some time and is well positioned to apply this proven framework to tradfi perpetual markets.

The Growth of On-Chain Equity and Commodity Perps

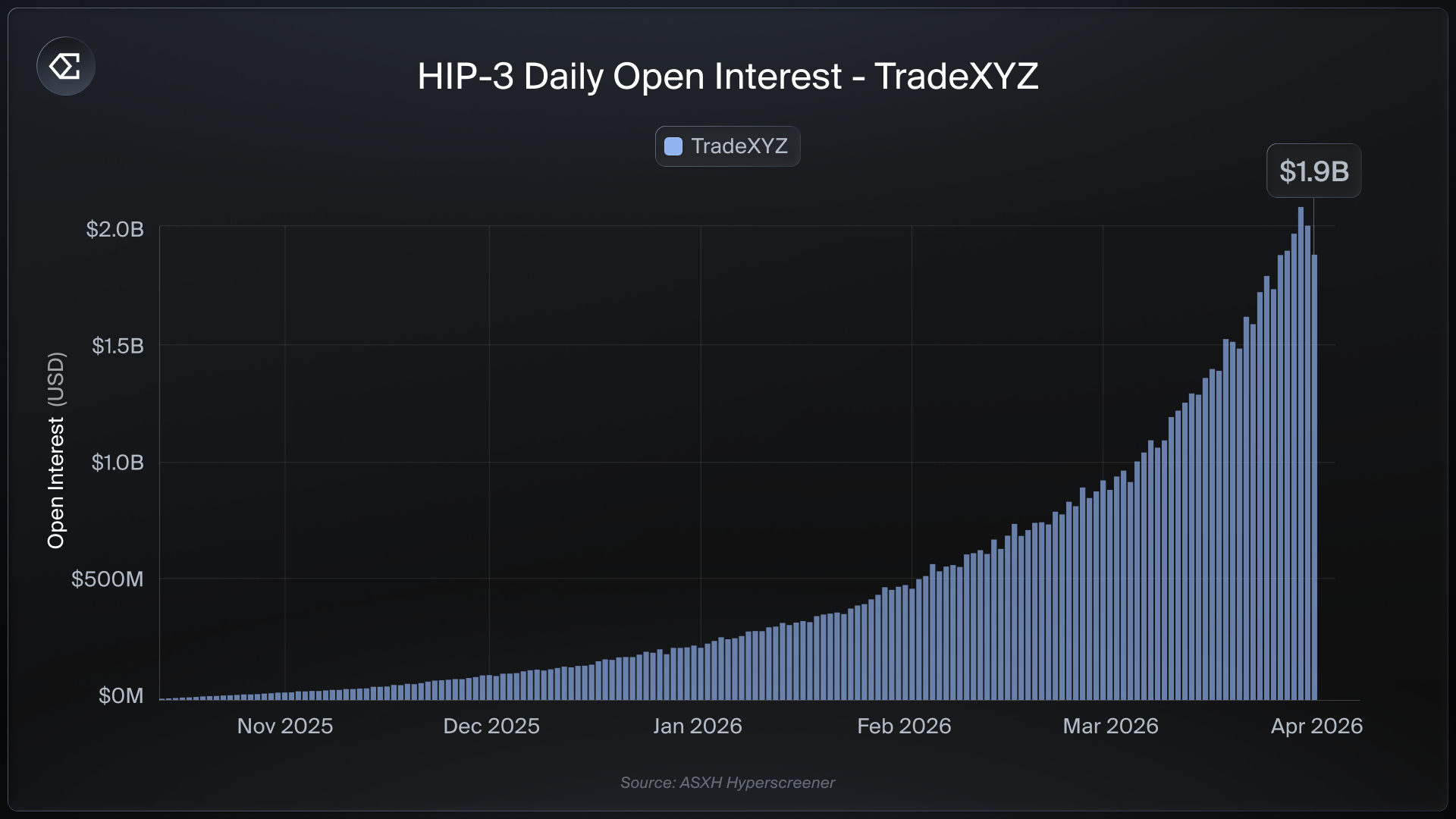

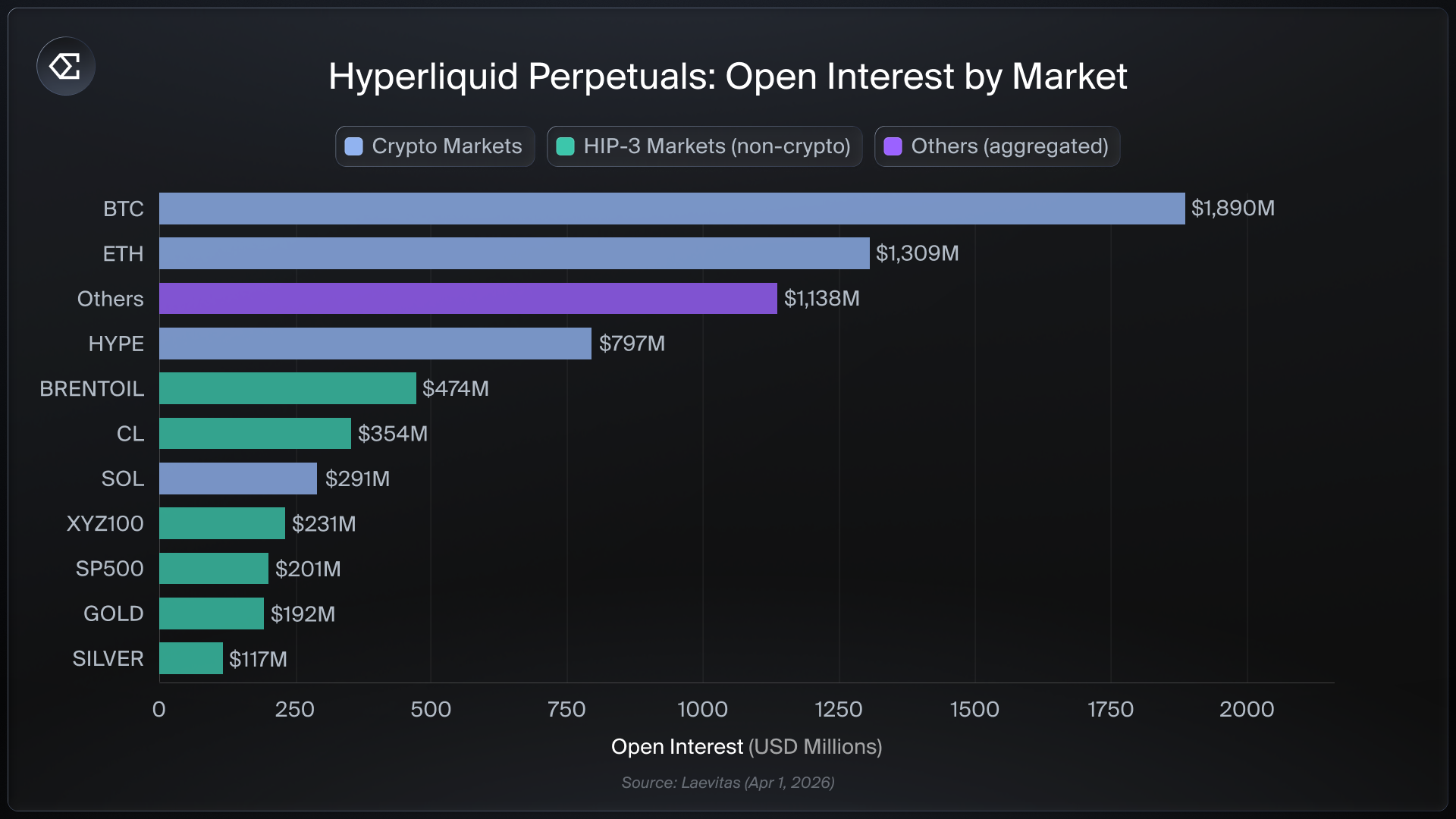

The on-chain equity and commodity perpetuals market has experienced rapid growth, driven primarily by Hyperliquid’s HIP-3 framework, which allows permissionless deployment of perpetual futures for any asset with a price feed. Since launching in October 2025, HIP-3 has grown from $70M in open interest to nearly $2B, primarily driven by trade.xyz

23 of the top 30 HIP-3 markets by open interest are now non-crypto pairs (equities, commodities, and indices) and 6 of the top 10 markets on Hyperliquid are non-crypto pairs.

Hyperliquid HIP-3 Open Interest. Source: Laevitas

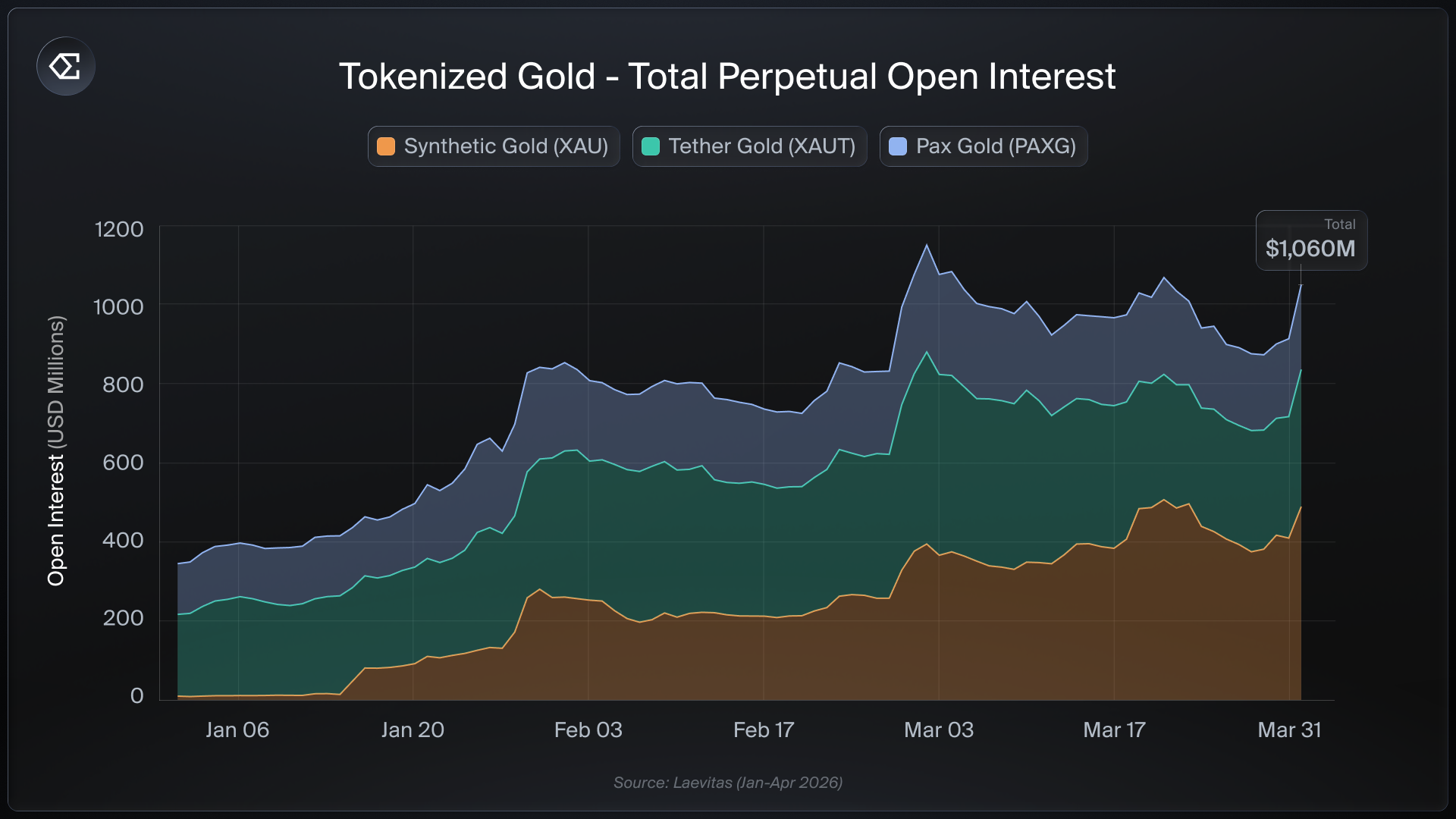

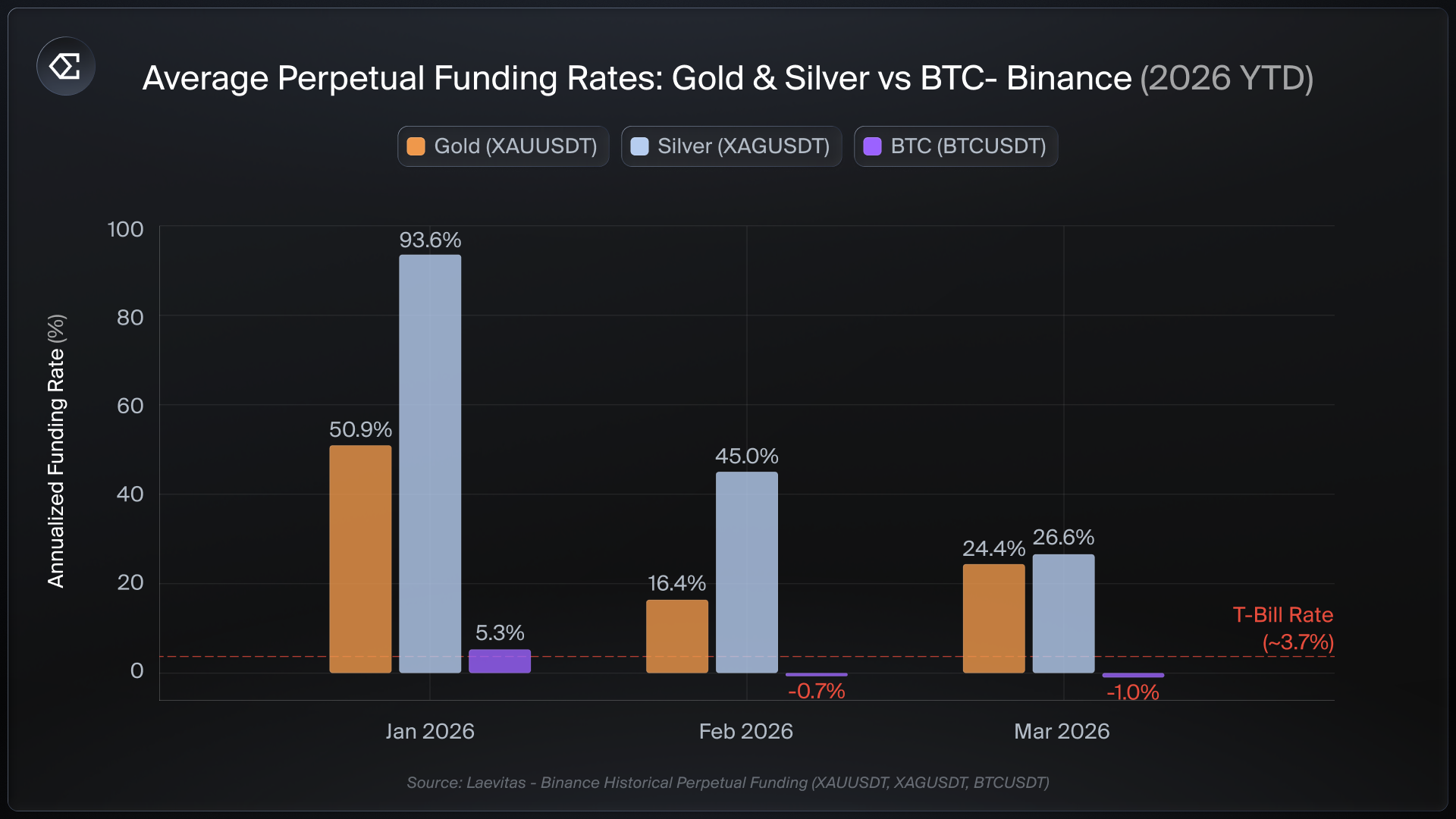

Commodity perpetuals in particular have become viable for basis trading, both from a funding rate perspective and from an open interest standpoint. Tokenised gold products on centralized exchanges, venues with which Ethena is already integrated, have surpassed $1bn in open interest, growing from $350m at the start of the year.

Funding Rates: A Basis Opportunity

Funding rates for commodity and equity perpetuals have remained elevated in 2026, reflecting strong long-side demand for exposure to gold, silver, and equity indices - particularly during periods of heightened geopolitical tension. This creates a basis opportunity for delta-neutral operators like Ethena, who can capture the funding rate differential by holding the spot asset and shorting the perpetual. For example, funding rates on Binance’s Gold perpetual future averaged 24.6% in March, which Ethena could capture.

Average Funding Rates for Binance perpetual future contracts. Source: Laevitas,

As with all new reserve categories, equity and commodity basis positions will be subject to allocation caps and risk parameters independently assessed and approved by the Ethena Risk Committee.

What Stays the Same

Each of the above initiatives will sit alongside the existing USDe backing to reduce concentration in any single strategy and build resilience across market cycles. The basis trade remains the core pillar of USDe’s backing, and the product’s fundamental architecture and redemption mechanism are unchanged.

Reporting and attestation infrastructure will scale with the backing’s composition, ensuring maintained or enhanced transparency - with Proof of Reserves staying unchanged and additional reporting initiatives to follow.

All initiatives have been, or will be, independently assessed and formally approved by the Ethena Risk Committee. The Risk Committee’s analysis is publicly available on our governance forum.

We are committed to operating within a defined, publicly disclosed risk framework so that the community can evaluate the guardrails and hold us accountable to them.